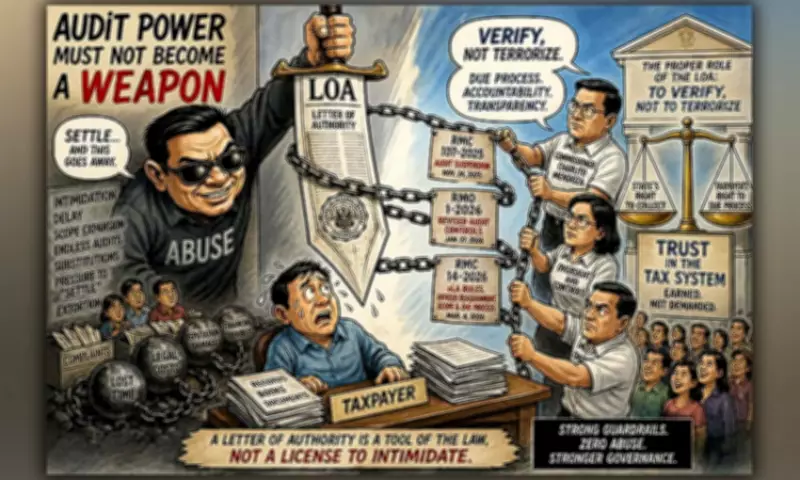

The Bureau of Internal Revenue's (BIR) Letter of Authority (LOA) is a legal tool designed to authorize tax audits, define their scope, identify authorized revenue officers, and protect due process by preventing arbitrary examinations. It is meant to safeguard both the state and the taxpayer.

However, when a safeguard itself becomes vulnerable to abuse, it can cease to provide protection and become a source of pressure. This danger is highlighted by longstanding allegations surrounding the misuse of LOAs—not as tools to verify compliance, but as instruments to intimidate, extract concessions, or wear down taxpayers through the burden of process.

The damage may already be done when a business, even one ultimately found compliant, is subjected to a prolonged or defective audit. From a taxpayer's perspective, an investigation can consume management time, raise legal and accounting costs, unsettle financing relationships, and harm a company's reputation. Coercion does not always come in the form of an explicit demand; sometimes it lies in the pressure to 'settle' simply to make the problem go away.

That is why BIR Commissioner Charlito Mendoza issued RMC 107-2025 on November 24, 2025. It suspended ongoing field audits and the creation, issuance, and service of new LOAs while the agency reviewed audit integrity. The suspension followed numerous complaints about audit abuses.

The reforms that followed matter for the same reason. On January 27, 2026, RMO 1-2026 was issued, revising audit controls. This was not simply bureaucratic housekeeping; it was an attempt to tighten procedures, reinforce oversight, and reduce opportunities for abuse.

Similarly, RMC 14-2026, issued March 4, 2026, clarified how tax audits would proceed after the 2025 audit suspension, particularly regarding the reassignment or substitution of revenue officers and the use of replacement electronic Letters of Authority (eLAs). It aimed to close loopholes that could enable abuse, including unauthorized substitutions, prolonged audits, and expansion of scope, while strengthening due process and restoring integrity to the LOA system.

The BIR responded to a deeper problem: audit power without strong controls invites misuse. The goal is not to weaken tax enforcement. The state has the right to collect lawful revenue and pursue evasion. But enforcement loses legitimacy when it appears selective, coercive, or corrupt. A tax system needs more than authority; it also needs trust that authority will not be misused.

That trust is fragile. An LOA should never be a bargaining chip, a threat hanging over businesses to compel silence or compliance unrelated to taxes, or a gateway for extortion. Its purpose is to verify, not to terrorize.

The lesson of the 2025 suspension and the reforms that followed is plain: even the government recognized that audit powers required stronger guardrails. That recognition should lead to more than internal circulars. It should lead to sustained transparency—clear audit timelines, stronger protections against repeated examinations, public reporting on disciplinary actions involving abuse, and strict accountability for officers who turn lawful authority into private leverage.

When taxpayers begin to fear the audit process more than they respect the tax system, the problem is no longer compliance. It is governance. And when an LOA becomes a letter of intimidation, the law has already been betrayed.